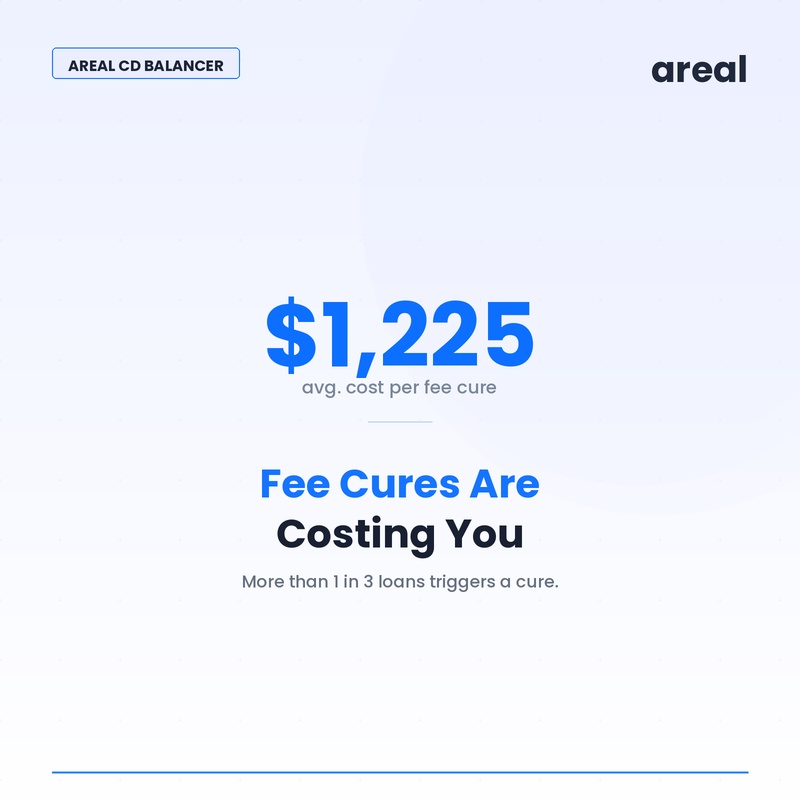

Fee Cures Are Costing Your Lending Operation $1,225 Per Loan. Here's the Fix.

More than one in three mortgage loans requires a fee cure. That's not a margin issue — it's a structural cost embedded in the way most lenders balance closing disclosures.

According to ICE Mortgage Technology's industry data, the average fee cure costs $1,225 per loan. For a lender closing 10,000 loans per year, that's over $4 million in annual cure costs — assuming a 33% cure rate. Lenders with higher cure rates or higher average cure amounts pay more. Significantly more.

The frustrating part: most fee cures are preventable. They don't come from unusual transactions or complex loan structures. They come from the manual process of reconciling Closing Disclosure fees between lenders and title companies — a process that's error-prone by design, not by exception.

What Is a Mortgage Fee Cure?

Under TRID rules established by the Consumer Financial Protection Bureau, certain fees disclosed on a borrower's Closing Disclosure cannot increase beyond specific tolerances without triggering a cure requirement. When fees exceed those tolerances, the lender must reimburse the borrower for the excess — the "cure."

The three tolerance buckets under TRID are:

Zero tolerance fees — These cannot increase at all between the Loan Estimate and the Closing Disclosure. Transfer taxes, recording fees for the lender's required documents, and most third-party services chosen by the lender from a provided list fall here.

10% aggregate tolerance fees — These fees can increase, but only if the cumulative increase across all fees in this category stays within 10% of the original Loan Estimate amounts. Third-party settlement services chosen from the lender's list, title insurance, and recording fees typically fall here.

No tolerance fees — These can change without triggering a cure. Prepaid interest, property insurance premiums, and certain escrow payments are in this category.

Most fee cures originate in the zero-tolerance and 10% tolerance categories — and most originate from a single, fixable source: errors in CD balancing.

Where Fee Cures Actually Come From

CD balancing is the process of reconciling the fees on a Closing Disclosure against what was originally quoted on the Loan Estimate. RESPA's tolerance rules govern how much certain fees can change between the LE and the CD — and when fees move outside those tolerances, a cure is required.

The most common sources of fee cures:

• Zero-tolerance violations. Fees that cannot increase at all — including origination charges and transfer taxes — are the highest-risk category. A $1 increase in a zero-tolerance fee triggers a cure.

• 10% tolerance violations. Third-party services and recording fees fall into a bucket where the total can increase by up to 10%. But calculating whether a group of fees has breached that threshold requires precise tracking across multiple line items.

• Late fee changes. Fees that change after the CD is issued — due to last-minute rate locks, escrow adjustments, or updated title charges — frequently trigger cures because the system doesn't flag the change in time for review.

• Manual entry errors. Incorrect fee amounts entered into the LOS, transposed numbers, and missed updates from third-party providers are the most preventable cause of cures — and among the most common.

The Cure Calculation: What It Actually Costs

The $1,225 average cure amount cited in industry studies reflects the direct cost of the cure itself — the amount the lender absorbs to bring fees back into compliance. But the full cost is higher when you account for operational overhead:

• Cure processing time. Each cure requires identifying the violation, calculating the correct amount, issuing a revised CD, obtaining updated borrower signatures, and documenting the resolution. Industry estimates put this at 2 to 4 hours of staff time per cure.

• Closing delays. When a cure is identified late in the process, closing may be delayed while the corrected CD goes through the required disclosure waiting period. A 3-business-day delay on a purchase loan has real consequences for buyers, sellers, and the lender's relationship with referral partners.

• Secondary market impact. Loans with documented fee cures may face investor scrutiny during purchase review. Some investors discount loans with cure histories, and repeated cures can affect a lender's seller/servicer standing.

For an operation closing 50 loans per month with a 5% cure rate, that's roughly 2 to 3 cures per month — adding up to $2,450 to $3,675 in direct cure costs, plus the operational overhead on top.

How Automated CD Balancing Eliminates Most Fee Cures

The root cause of most fee cures isn't intent — it's the gap between when fees are entered and when they're checked against tolerance rules. In a manual process, that check happens at the end, when it's too late to adjust without triggering a delay.

Automated CD balancing shifts that check to the beginning. Areal's CD Balancer applies tolerance rules in real time as fees are entered and updated, flagging potential violations before the CD is issued rather than after.

How it works in practice:

• Real-time tolerance monitoring. As fees are added or updated, the system calculates running tolerance buckets and flags any fee that would breach a zero-tolerance or 10% limit.

• Automatic change detection. When third-party fees update — from title, settlement, or escrow providers — the system identifies the change and reassesses the tolerance position automatically.

• Pre-disclosure validation. Before a CD is issued, the system runs a final tolerance check and flags any items requiring review. Closers see the issues before the borrower does.

• Audit trail. Every fee change and tolerance calculation is logged, creating a defensible record for regulatory review or investor due diligence.

The result: lenders using CD Balancer see fee cure rates drop to near zero on the violations that automation can catch — primarily entry errors, late fee changes, and miscalculated tolerance buckets.

Getting Started: Where to Focus First

Not every fee cure comes from the same source, and the fix isn't the same for every operation. The first step is understanding where your cures are coming from.

Pull 90 days of cure data and categorize by type: zero-tolerance violations, 10% bucket breaches, and late changes. That breakdown tells you whether the problem is primarily a data entry issue, a third-party fee update issue, or a process timing issue — and which of those your current tools are equipped to handle.

If the majority of your cures are coming from entry errors and late changes — the most common pattern — automated CD balancing addresses them directly. If you're seeing zero-tolerance violations from fees that were correctly entered but changed after locking, the problem is upstream: fee change notification from your third-party providers.

Either way, the analysis is worth doing before you invest in tooling. Automation that targets the right failure mode will have measurable impact. Automation that doesn't match your actual cure pattern won't.

Areal's CD Balancer was built specifically for mortgage closing operations, and it's designed to connect with the LOS and third-party fee systems your team already uses. If you're running more than a handful of cures per month and want to understand what's driving them, we're worth a conversation.

AREAL READING

Read resources written by professionals.

Don’t miss any update about Mortgage and Title Industry

Read more